The Fed Is on Thinner Ice Than It Realizes, and It May Be Setting Us Up for Recession

The Fed Is on Thinner Ice Than It Realizes, and It May Be Setting Us Up for Recession

Have members of the Federal Reserve already engineered a soft landing?

And are they even asking that question?

The thought came to me while reading Barry Ritholtz’s recent piece on policy normalization:

I believe monetary policymakers generally concur with Ritholtz. They see zero interest rates as an artifact of the financial crisis. The economy today resembles normality—and so, too, should monetary policy. Hence the push to raise rates this year, possibly as early as the next meeting in September.

Consider instead that zero—or at least, very low—short-term rates reflect the realities of the new normal for economic growth. In this scenario, quantitative easing was the Fed’s emergency policy setting. And by ending quantitative easing, the Fed has already normalized policy.

Monetary policymakers will resist this interpretation. They do not believe that tapering and ending the bond-buying program reflects a tightening of policy.

Regardless of what they believe, however, real interest rates rose at the suggestion that QE has a short half-life:

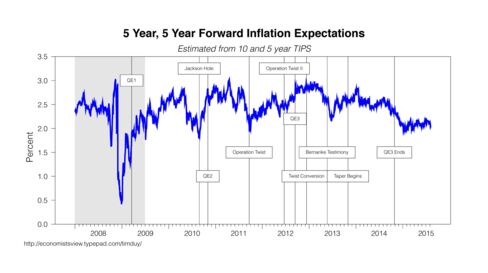

Meanwhile, inflation expectations have waned:

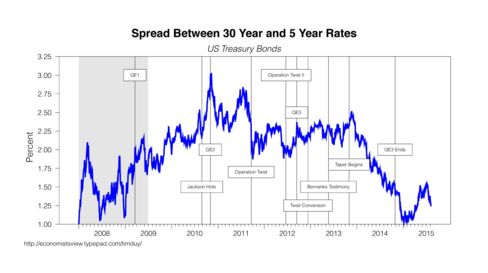

And the yield curve has flattened:

Equities started moving sideways after QE ended:

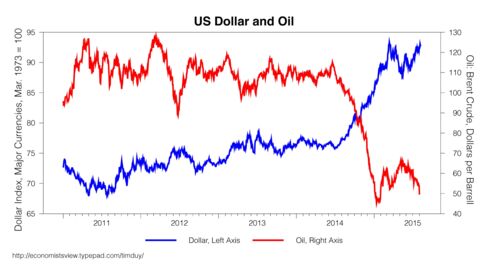

The dollar rose and oil cratered as the end of QE approached:

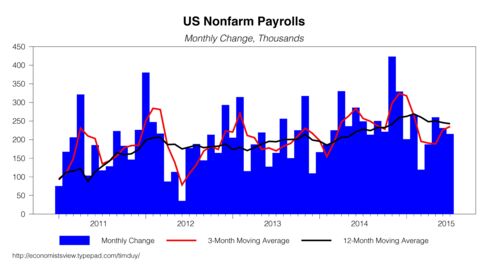

Meanwhile, employment gains stabilized:

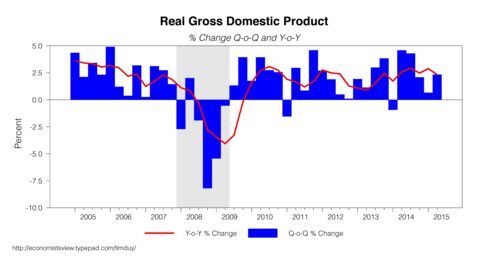

As did gross domestic product growth:

Moreover, the effects spread outside U.S. borders.

David Beckworth argues that China is yet another victim of the Fed’s status as a monetary superpower. And it should not go unnoticed that as the economy has settled into this mediocre equilibrium, fears of inflation or widespread wage acceleration remain premature—arguably, almost as if the Fed pulled the plug a little too early.

The Fed doesn’t see things this way. It doesn’t believe it has engineered the soft landing just yet. It expects that interest rates will need to rise farther to tame inflationary pressures. In fact, the Fed believes that the economy will evolve in such a way that it can raise short-term rates back to levels comparable to the old normal.

Financial markets participants, however, are not on the same page. They see the Fed staying persistently lower than Federal Open Market Committee meeting participants anticipate.

I would argue that financial markets are signaling that a soft landing has already been achieved and that much additional tightening will risk tipping the economy back into recession. The Fed staff is stuck in between; at least that is the story told by theaccidental release of staff forecasts. The staff envisions a near-term policy path that better resembles what is expected by financial markets, although the staff, like FOMC participants, can’t shake its faith that eventually rates will return to something more like the historical norm.

Gavyn Davies, a former Goldman Sachs economist now at Fulcrum Asset Management, sums up the situation nicely:

Ultimately, it is of course the FOMC, not the staff, that matters for policy. In the run up to … [last month’s] policy meeting, the key members of the FOMC have seemed fairly determined to announce lift off in September. But, after that, it is debatable how far they will push their hawkish view of the appropriate path for the equilibrium rate, when they have both the markets and their own economics staff against them.

This, I think, is right.

My concern now is that the FOMC is on thinner ice than members realize because they don’t believe they have already tightened policy. The soft landing may already be upon us. They just don’t know it, or won’t admit it.

That’s a recipe for recession.

Add comment